A Gary Alpert Financial Strategies Case Study

This is a hypothetical situation based on real-life examples. Names and circumstances have been changed. The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investments or strategies may be appropriate for you, consult your advisor prior to investing. (150-LPL)

Let's TalkKristen spent more than 25 years building her career at a Fortune 100 retailer, rising into an executive role that came with all the perks and complications: strong income, meaningful equity compensation, and a growing stock position that “worked” — right up until the day it became a risk she could not ignore.

Like a lot of high achievers, Kristen did what smart, capable people often do when life gets busy: she handled things as they came. Her stock awards kept vesting. She kept holding. Her portfolio became increasingly concentrated in one company, and the deeper she got, the harder it felt to unwind without creating a tax mess.

Then retirement showed up earlier than most. Not 65. Not even 60. Kristen retired in fall 2024 at 57, with a new life in South Carolina, a son living out of state, and a long runway ahead. She did not need more “investment talk.” She needed a real plan — one that protected what she built, made retirement feel predictable, and lowered the risk of one wrong move in the market taking a chunk out of her future.

That’s where our team at Gary Alpert Financial Strategies entered the picture.

A business brings a lot of paperwork. On top of that, you've got to manage your taxes. We take care off everything for you.

A business brings a lot of paperwork. On top of that, you've got to manage your taxes. We take care off everything for you.

A business brings a lot of paperwork. On top of that, you've got to manage your taxes. We take care off everything for you.

Kristen's situation looked great on paper. She had accumulated several million in investable assets, carried no debt, and was in strong financial shape.

Stock Accumulation

A major stock concentration tied to both her portfolio and her former employer.

Timing

A tax picture that could change dramatically depending on how and when stock was sold.

Complexity

A retirement transition full of time-sensitive decisions.

Uncertain Future

A single-person household with estate planning and long-term care questions.

In other words: nothing was broken — and that’s what made it time-sensitive. When risk remains abstract rather than immediate, it’s easy to postpone the hard decisions.

Kristen knew the concentration was a problem. She just had never seen a compelling reason to fix it… until retirement became less of a dream, and more of a certainty. At this point it became clear that it was time to think differently.

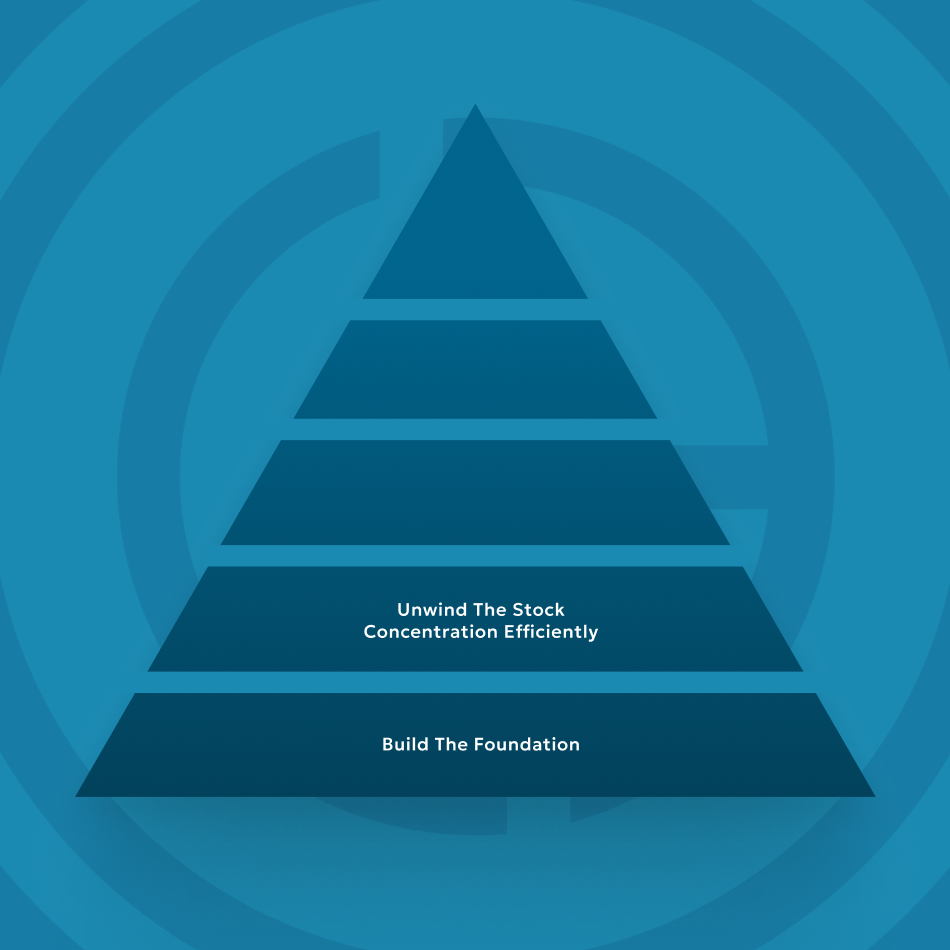

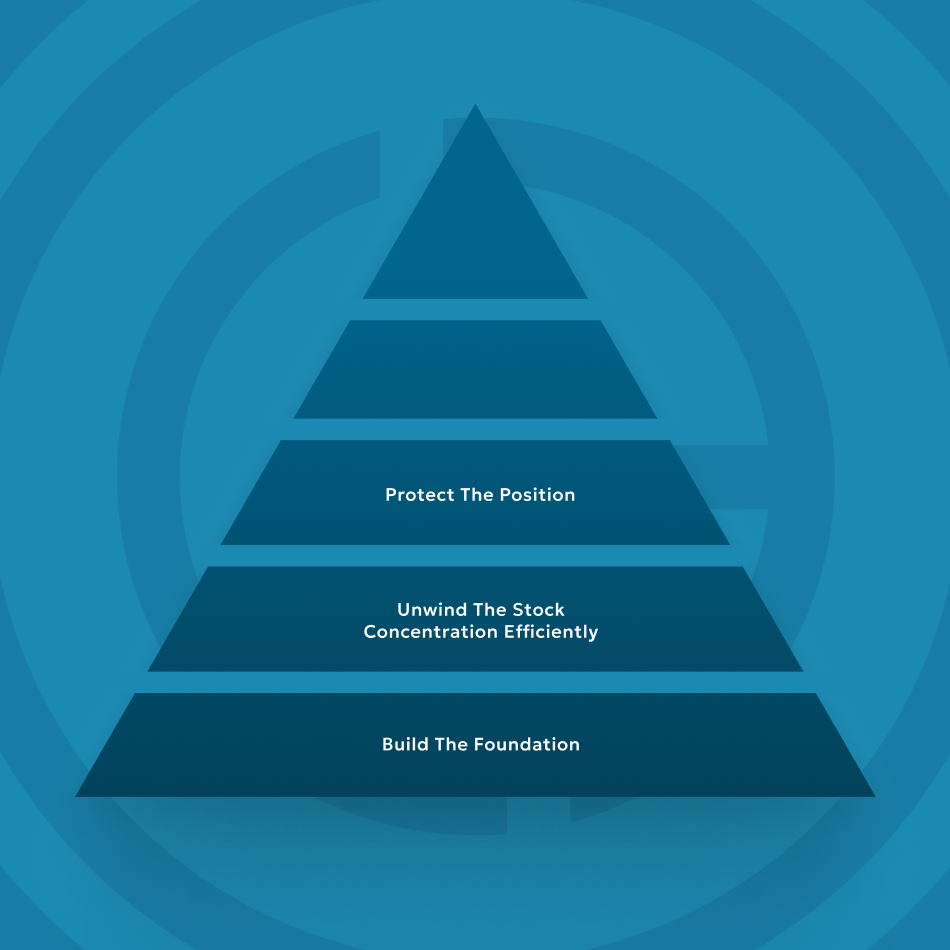

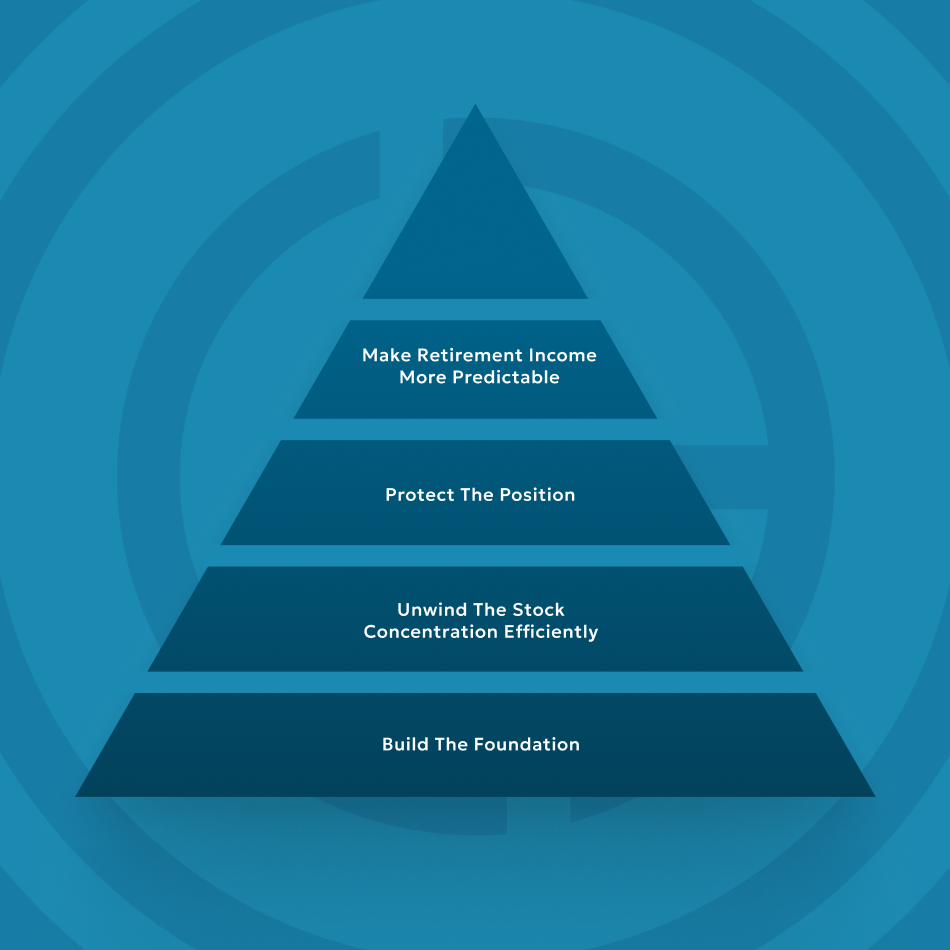

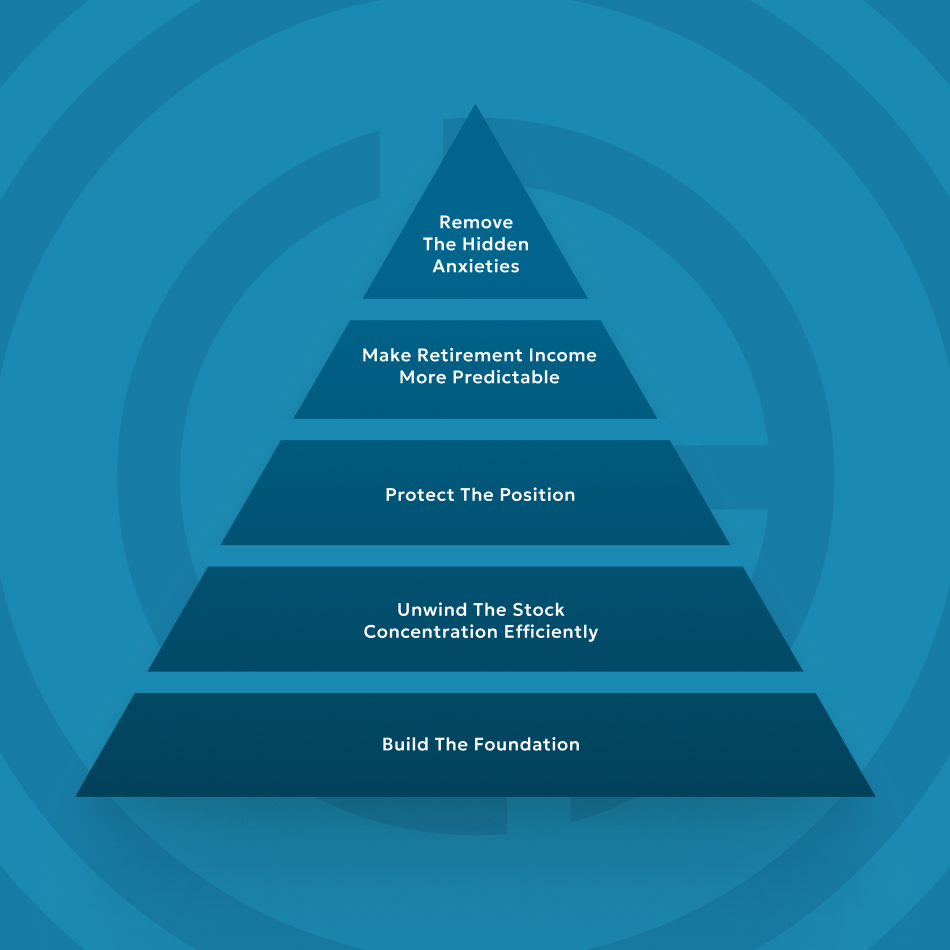

1. Stop the concentration from growing.

A big early win came through education. Kristen held on to vested restricted stock because it felt simpler, and selling felt like it might create extra tax consequences. Our team walked her through the reality: once stock vested, she had flexibility to sell without triggering additional income tax beyond what was already recognized at vesting. That insight alone helped change behavior and slow the accumulation.

2. Build a tax-smart exit plan for the legacy stock.

Reducing a large stock position is not as simple as “sell it.” The timing matters because the tax impact can swing dramatically based on income thresholds.

Using scenario modeling, our team stress-tested six scenarios with different sale timing/amounts to answer one question:

How much stock could Kristen sell each year to meaningfully reduce risk while staying in a more favorable capital gains range?

This mattered because the wrong move could push her into higher effective capital gains rates and trigger additional taxes that appear only after certain thresholds are crossed (including the Net Investment Income Tax).

The team’s plan focused on using Kristen's post-retirement “low-income window” — a two-year stretch where ordinary income dropped enough to make strategic sales far more efficient. The goal: reduce the concentration before distributions from qualified accounts begin, and do it with discipline instead of guesswork.

Kristen is an ideal example of who Gary Alpert Financial Strategies serves best: high-achieving professionals approaching a transition point — retirement, liquidity events, equity compensation complexity — who want more than market commentary.

They want structure and discipline.

They want a planning process that works regardless of headlines.

They want a partner who will be with them for the long haul.

This case study isn’t about one stock position or one retirement date. It’s about what happens when a capable person stops improvising and starts working with a team that can simplify the complex, help protect the downside, and build a repeatable path forward.

We believe it’s time to think differently. We want your life after work to feel intentional, stable, and genuinely fulfilling. Reach out to us today if that sounds like a good plan for you and your family.

Reach out today and let’s explore how we can bring clarity and calm to your financial life.

Fill out the form below, and we'll get back to you shortly.

.png)